Boost Your Business Cash Flow with Invoice Financing: Here’s How

Get a Personal Loan in 2 mins

Quick approval, minimal documents, and flexible repayment options

Share with your community!

Running a small or mid-sized business often feels like walking a tightrope—especially when your cash flow is stretched thin. You’ve completed a big order, your clients are happy, but your money is stuck in unpaid invoices. Meanwhile, bills don’t wait. Payroll needs to go out. Suppliers are calling. And you’re wondering, how do I keep things moving?

That’s where invoice financing steps in. It’s not some complex financial tool reserved for large enterprises. In fact, it’s designed to help businesses like yours turn unpaid invoices into instant working capital.

Let’s unpack how invoice financing works and how it can help you keep your cash flow smooth, even when clients are slow to pay.

What is Invoice Financing?

Invoice financing also known as invoice factoring or an accounts receivable loan is a way for businesses to get immediate funds based on their outstanding invoices.

Here’s the simple version:

You issue an invoice to a client for a service or product delivered.

Instead of waiting 30, 60, or even 90 days for payment, you approach a financing company.

They give you a major portion (usually 70–90%) of the invoice amount upfront.

When your client eventually pays, you receive the remaining amount—minus a small service fee.

So essentially, it’s a business cash flow loan tied directly to your receivables.

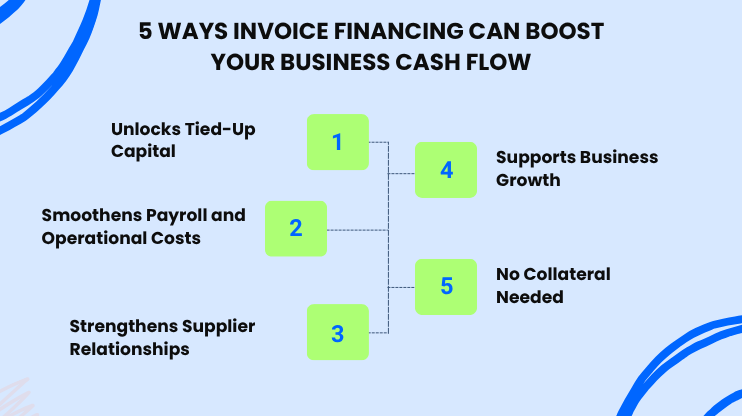

Why SMEs Choose Invoice Financing

Traditional loans require credit checks, lengthy paperwork, and sometimes collateral. But with invoice financing, your receivables become the asset.

Here’s why it’s popular among SMEs:

No need to wait on client payments to get funds.

No need for perfect credit scores—the focus is on your client’s payment ability.

Quick approval and disbursal, often within 24–48 hours.

Keeps your equity safe—it’s not like selling off a stake or taking a long-term loan.

For businesses in manufacturing, services, wholesale, or logistics, invoice financing can be a game-changer.

Not all providers are the same. Here’s what to look for:

Transparent fee structure: No hidden charges or fine print surprises.

Industry experience: They should understand your sector and typical invoice cycles.

Flexible terms: Can they scale with your business as you grow?

Good support team: Fast response when you need help is a must.

Pro tip: Always read the agreement carefully and ask questions—especially about recourse vs. non-recourse factoring.

Final Word

Invoice financing isn’t just a band-aid for cash flow stress—it’s a strategic tool for growing businesses. If your money is stuck in unpaid invoices, this could be the key to unlocking it and fueling your next big move.

Whether you call it invoice factoring, an accounts receivable loan, or simply a way to boost your business cash flow—the value is real.

Explore how Instalment Express helps you manage sudden medical expenses in India. Quick approval, flexible repayment, and hassle-free healthcare financing.

Explore how Instalment Express helps you manage sudden medical expenses in India. Quick approval, flexible repayment, and hassle-free healthcare financing.